How much does freight factoring really cost a 3-truck fleet?

A 3-truck fleet factoring $20,000 a week at 3% pays closer to $3,200 a month once transfer fees, funding charges, and contract minimums stack up. Here's the real math.

How much does freight factoring really cost a 3-truck fleet?

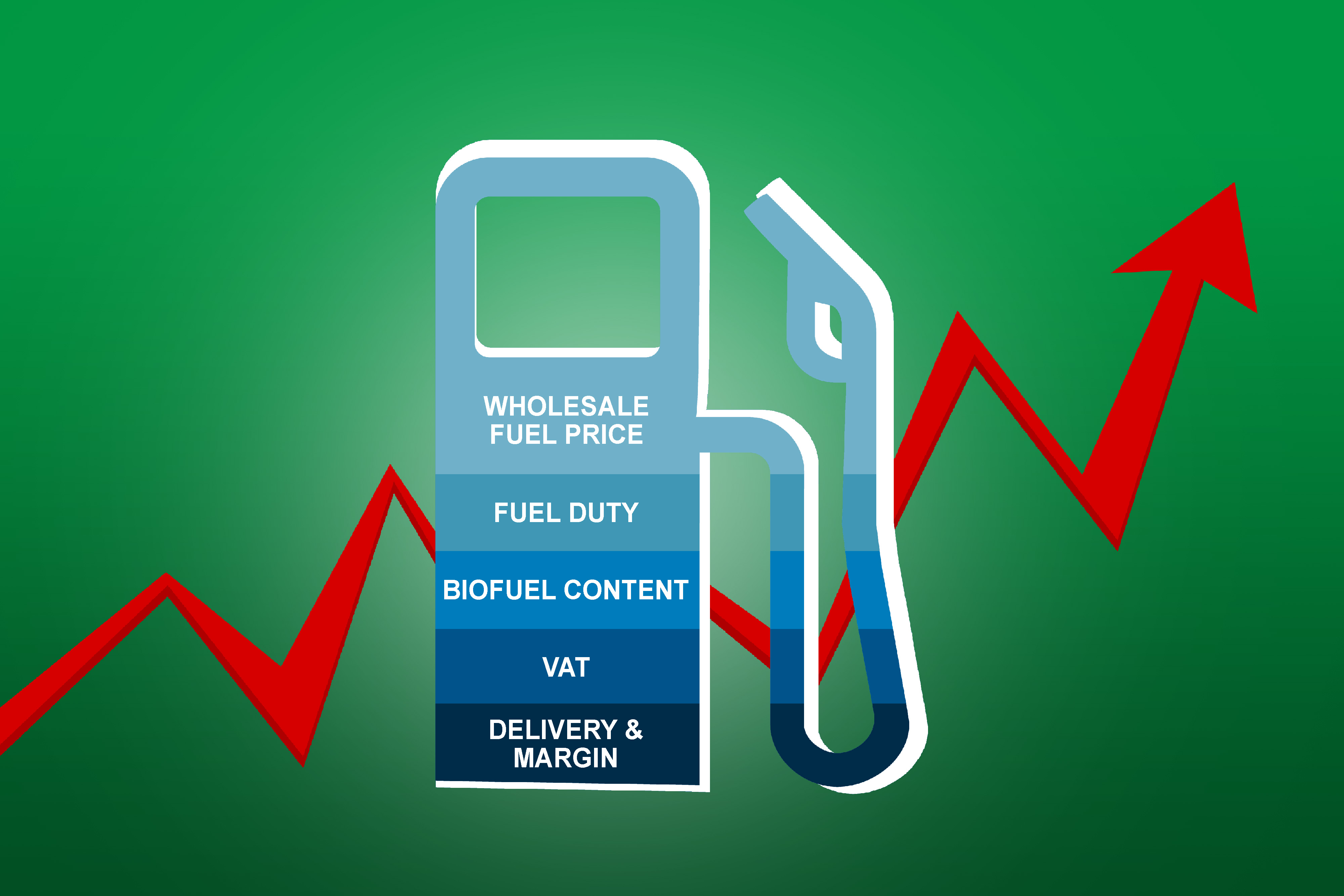

A carrier factoring $20,000 per week at a 3% rate pays $600 per week in discount fees. That's $2,400 a month. But the real monthly cost climbs to $3,200 once you add transfer fees ($10 per invoice, 20 invoices = $200), same-day funding charges (0.5% per invoice = $400), and monthly minimums ($200). The advertised rate is only part of the bill.

The discount rate: recourse vs. non-recourse

Factoring companies charge a percentage of the invoice value. That percentage is the discount rate. Recourse factoring (where you take the risk if a broker doesn't pay) runs 1% to 3%. Non-recourse factoring (where the factor assumes the risk under specific conditions) runs 2% to 5%. The difference reflects who holds the bag when a broker goes under or disputes a load.

Flat rate vs. tiered pricing

Flat-rate factoring charges the same percentage regardless of how long the broker takes to pay. Tiered pricing starts lower but adds increments for every 10 or 15 days beyond the first period. If a broker pays in 50 days and your contract is 2% for the first 30 days plus 1% per additional 10-day period, you pay 2% + 1% + 1% = 4% total. Tiered structures look cheaper up front but cost more when brokers stretch payment past 30 days, which happens often in trucking.

Spot vs. contract factoring

Spot factoring (occasional use) costs 3% to 6% per invoice with no commitment. Contract factoring (ongoing relationship) costs 1.5% to 4% but requires you to factor all invoices or hit a monthly minimum. The difference comes down to predictability. A factor modeling your volume and broker mix every week can price lower than one funding a single load with no history. If you factor every week, you're already operating like a contract client but paying spot-level pricing.

Transfer fees

Most factoring companies charge a fee every time they send funds. ACH transfers run $2 to $15 per transaction. Wire transfers run $10 to $35. On 20 invoices a month at $10 per transfer, that's $200 on top of your discount rate. Over a year, $2,400.

Same-day funding charges

Some companies promote fast funding but charge extra for same-day access. The fee shows up as 0.25% to 1.0% per invoice or as a flat charge per transaction. On a $3,000 invoice, 0.5% is $15. Across 20 invoices a month, that's $300. Your effective rate climbs from 3% to 3.5% or higher.

Monthly minimums and volume penalties

Certain contracts require you to factor a minimum dollar amount each month. If you don't hit it, you pay a penalty ranging from $250 to $1,000 or more. For carriers with inconsistent volume, this creates a hidden cost during slow months when cash flow is already tight. Your effective rate increases exactly when you can least afford it.

Early termination fees

Some agreements include cancellation fees if you exit before the contract term ends. These range from $500 to $5,000 or more. A competitive rate loses value fast if it locks you into a costly agreement you can't leave without paying a penalty.

Setup and credit check fees

Some factors charge for onboarding or evaluating new brokers. Credit checks typically cost $10 to $50 per customer. Setup fees range from $100 to $500. These aren't always significant on their own, but they add to the total cost of doing business.

Chargebacks: the cost you don't see coming

One of the most important costs in factoring is not listed as a fee. It appears when an invoice is funded but later charged back to the carrier. This is common in recourse programs and can still happen in limited non-recourse structures if a broker doesn't pay, disputes the load, or becomes insolvent. If a factor advanced 90% on a $3,000 invoice, the carrier may need to return $2,700 out of pocket. Understanding when a chargeback can happen matters as much as the rate.

Real-world example: $20,000 per week

A carrier factors $20,000 per week at a 3% rate. At first glance, the math is simple: $20,000 × 3% = $600 per week, or approximately $2,400 per month. Now layer in the operational costs:

- Transfer fees: $10 per invoice × 20 invoices = $200

- Same-day funding: 0.5% per invoice × $20,000 per week × 4 weeks = $400

- Monthly minimum shortfall (one slow week): $200

The real monthly cost is no longer $2,400. It comes out closer to $3,200 per month. A carrier may think they are paying 3%, when the real monthly cost is closer to 4% once transfer fees, funding fees, and contract-related charges are included.

George McWilliams, VP of Business Development at Summar Financial, put it this way: "That 1% on a thousand bucks can turn to 6, 7% by the time you've factored everything in."

At $50,000 in monthly invoices, the gap between 3% and 4% is $500 per month, or $6,000 per year.

When factoring pays for itself

Without factoring, you wait 30 to 45 days to get paid. Fuel, maintenance, and growth all depend on available cash or credit. In many cases, that leads to relying on credit cards or short-term loans, which introduce interest costs and repayment pressure.

With factoring, you convert invoices into immediate liquidity. If factoring costs $3,000 per month but allows you to run two additional loads per week at $400 profit per load, the math works: 2 loads × 4 weeks × $400 = $3,200. In that scenario, factoring offsets its own cost. If it doesn't help you increase revenue, reduce operational stress, or improve consistency, it may not be the right tool.

The question to ask before signing

Two factoring companies can quote the same rate and deliver completely different real costs. One may rely on transfer fees, funding charges, minimums, or contract penalties that only surface once the relationship is underway. Another keeps pricing simple and predictable from the start. That difference determines whether factoring becomes a tool for growth or an expense that keeps quietly rising over time.

The question worth asking before signing is not just "what is your rate?" It is what exactly is included, what is not, and what will this relationship actually cost once you are running loads every week. The factoring company that answers those questions clearly and upfront is almost always the better long-term partner, regardless of where the initial rate lands relative to the competition.

For more on what a 3-truck fleet needs to qualify for freight factoring, see what does a 3-truck fleet need to qualify for freight factoring.